Note: This is an updated version of this blog: Putting The Pieces Together: An Often-Overlooked Part of the Investing Puzzle. Some additional information is also provided.

ASSET LOCATION

A common real estate mantra is “location, location, location.” While some are unaware and others don’t consider it, location matters to investors, too.

When it comes to investing, there are two types of diversification:

- Asset diversification

- Asset location

You diversify your assets by holding different types of assets. This means holding stocks and bonds. It includes holding U.S.- and non-U.S.-based assets. It also involves holding assets of various sizes and with different objectives.

To the extent possible, you also want to have a different type of diversification. You want to hold your assets in different types of accounts from a tax perspective. That’s what asset location is all about.

Asset location refers to what type of account an investment is held in from a tax perspective. You can hold investments in tax-deferred accounts (e.g., Individual Retirement Accounts or IRAs), taxable accounts, or tax-exempt accounts (e.g., Roth IRAs). You can also hold them in Health Savings Accounts, which provide a triple-tax benefit. Paying attention to asset location can improve your portfolio’s after-tax returns. For every additional dollar your portfolio earns, you can save one dollar less – or spend one dollar more later.

Investors more commonly focus on asset allocation and/or diversification. Many studies show the way you diversify your assets across different asset classes drives your investment returns. Asset allocation also helps reduce risk. In short, we do not want to “put all our eggs in one basket.” If we diversify, we can increase the likelihood of achieving our long-term goals. We can also enhance our potential to realize long-term gains.

ACCOUNT VS. HOLISTIC

Many advisors manage portfolios and implement financial plans at the account level. This means they manage each account separately rather than taking a collective view. Account-level management typically puts a full allocation of investments into each account. As a result, clients with a 60/40 asset allocation model have the same investments in the same percentages in each of their accounts, i.e., taxable accounts, IRAs, Roth IRAs, etc.

This approach makes it much easier to manage a client’s assets. But it has some disadvantages for clients who hold assets in both taxable and tax-deferred accounts. Failing to locate specific investment types among account types can reduce the tax efficiency of your portfolio. For example, when buying or selling a new security, you may buy or sell it in each account. If choosing what assets to hold in a 401(k) account with limited options, you may have to select an inferior choice to maintain the desired diversification parameters. Failure to pay attention to asset location may also increase your overall tax bill.

At Apprise, asset location matters. It is an important consideration for every client. For some clients, asset location is not possible initially. Why? They hold all their retirement assets in a workplace 401k. If that’s the case, we look for opportunities to start a Roth IRA, a taxable brokerage account, or a Health Savings Account.

Unfortunately, we cannot make a definitive ranking of the type of investments to place in tax-deferred accounts. Why? Several changeable factors can impact such ranking:

- Tax rates. – These can change due to the political environment as well as an investor’s income level.

- Investment Holding Periods. – These can be specific to the investor and the strategy she implements.

- Return Parameters. – These are constantly in flux as they are affected by the economy as well as market performance.

Factors Affecting Asset Location

You should consider the following factors when deciding the type where to locate an investment.

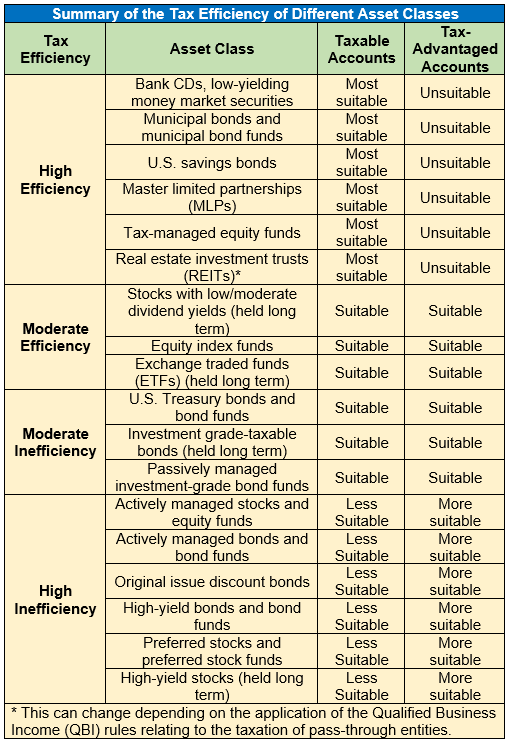

- Can you place the investment in a tax-deferred account? Unfortunately, you cannot own all investment types in tax-deferred accounts. For example, under the tax code, you cannot own collectibles in IRAs. There are some exceptions related to precious metals, including certain gold and silver coins issued after 1986, along with silver, platinum, and palladium bullion.

- Taxation of Interest. While there are some exceptions (e.g., municipal bond income), most interest is taxable as ordinary income.

- Taxation of Capital Gains. You realize a capital gain when you sell or exchange an investment for more than the purchase price. Short-term capital gains get taxed as ordinary income. They arise when you sell investments held for a year or less. Long-term capital gains result from the sale of an asset held for more than one year. The tax rate for long-term capital gains is lower than the investor’s ordinary income tax rate.

- Taxation of Capital Losses. You realize a capital loss when you sell or exchange an investment for less than its cost basis. In taxable accounts, capital losses offset any capital first. Short-term gains and losses get combined, leaving you with a net gain or loss. Then you follow the same process for long-term gains and losses. If capital losses exceed gains, you can deduct up to $3,000 of such losses annually. You can carry unused capital losses until used. Generating a capital loss in a tax-deferred account provides no tax benefits.

- Taxation of Dividends. Qualified dividends are paid out of corporate earnings and receive the same preferential tax rate as long-term capital gains. But not all dividends are qualified. For a dividend to be qualified, it must have been paid by a U.S. corporation or a qualified foreign corporation. You must also own the stock for more than 60 days during the 121-day period that begins 60 days before the stock’s ex-dividend date. Dividends from tax-exempt corporations or organizations that generally are not subject to income tax are non-qualified. They generally get taxed at the same rate as ordinary income. (See below for special rules related to dividends paid by Real Estate Investment Trusts – REITs.)

- Foreign Taxes Paid. If you own non-U.S.-based securities, you may pay withholding tax on any dividends you receive. If you hold the shares in a taxable account, you can claim either a credit (dollar-for-dollar reduction in taxes) or a deduction for the withholding tax when you file your tax return. Please note that only income taxes, which include withholding taxes, qualify for credit on your U.S. tax return.

- Dividends Paid by Real Estate Investment Trusts (REITs). REIT dividends are considered pass-through income to the shareholder. This allows them to qualify for the qualified business income or QBI deduction. This deduction was created as part of the Tax Cuts and Jobs Act of 2017. It went into effect in the 2018 tax year. The QBI deduction allows you to deduct the lesser of: 20% of your qualified business income (QBI), plus 20% of qualified real estate investment trust (REIT) dividends, and qualified publicly traded partnership (PTP) income, or 20% of your taxable income minus net capital gain.

- Tax-Deferred Accounts. Tax-deferred accounts allow a taxpayer to delay paying taxes on assets contributed to the account until some future date – typically when the assets are withdrawn. Examples of tax-deferred retirement savings accounts include 401(k), 457, and 403(b) plans for employees as well as Keogh plans for self-employed individuals. These plans allow you to contribute a percentage of your pre-tax salary into one or more investment accounts. This provides tax-free growth. Regular or traditional IRAs are also tax-deferred accounts.

- Tax-Deferred Assets. Tax-deferred assets allow a taxpayer to defer at least some of the income the asset generates.

- U.S. Savings Bonds. Owners of U.S. savings bonds can wait to pay taxes until they cash in the bond, when the bond matures, or when they transfer the bond to another owner.

- Master Limited Partnerships (MLPs). If you own shares of a master limited partnership, you can take advantage of the tax deferral embedded within its structure. MLPs can use depreciation to offset distributed cash flows. This causes the taxable amount they distribute to unitholders to be lower than the actual cash distribution. Untaxed distributions can also result in a reduction in your basis in the shares. (This means you reduce what you paid for the shares by the amount of this distribution. As a result, when you sell shares of an MLP at a gain, some of the gains will be taxed at the lower capital gains rate.

- Tax-Exempt Status. Tax-exempt refers to income earned or transactions that are free from taxation. Examples of tax-exempt retirement accounts include Roth 401(k), Roth 403(b), and Roth IRA accounts. You fund such accounts with after-tax dollars. These provide future benefits. Withdrawals taken following a five-year period after contributions to the account have been made, and generally, after the account owner is at least age 59 ½, are not subject to taxes.

- State and Local Taxes. Some securities are exempt from federal and/or state taxes.

- Municipal Bonds. Interest income received from investing in municipal bonds is free from federal income taxes. In most cases, interest income investors receive from securities issued by municipalities within their state of residence is also exempt from state and local taxes. Interest income from bonds issued by U.S. territories and possessions is exempt from federal, state, and local income taxes in all 50 states.

- Interest Income from Treasury Bills and U.S. Savings Bonds. You pay federal income taxes on interest income earned from Treasury bills, notes, and bonds. But you do not pay state and local income taxes on such amounts. Similarly, you pay federal income tax on income from U.S. savings bonds. You do not pay taxes on this income at the state or local level.

Other Tax-Exempt Accounts:

- 529 College Savings Plans. The 529 savings plan is also a tax-exempt account. You contribute after-tax dollars to the account. However, you pay no taxes on portfolio earnings provided you use the funds for educational purposes. Many states also allow taxpayers to deduct contributions to such accounts.

- Health Savings Accounts (HSAs). You can make tax-deductible contributions to HSAs. You can withdraw amounts that reimburse qualified medical expenses tax-free as well. Assets held in such accounts can also generally grow tax-free.

Some Advantages of Asset Location

You should try to hold tax-inefficient investments in retirement accounts, tax-efficient investments in taxable accounts, and high-return investments in Roth IRAs. Why? Appreciating investments held in an IRA will get taxed at ordinary income rates upon withdrawal. This treatment will even apply to your heirs.

If held in a taxable account, appreciation in your assets does not get taxed unless and until you sell the asset. In that situation, capital gains tax rates, which are lower than ordinary income tax rates, apply. Therefore, holding appreciating investments in retirement accounts is like telling the government it is okay to potentially pay much more in taxes.

Another advantage: If you are a long-term buy-and-hold investor and do not need to sell appreciated assets held in taxable accounts during retirement, your heirs will benefit. Under current law, the basis in such assets gets stepped up to fair market value when you die. Your beneficiaries could potentially pay no tax at all when selling the asset.

Holding tax-inefficient investments, such as U.S. bonds, in a retirement account, effectively defers any taxes until you start drawing down the account. Although this will result in ordinary tax when earnings are realized, the income would have been subject to ordinary tax anyway. While you can hold municipal bonds in a taxable account, they still typically provide less income. Also, fixed-income investments tend to produce lower long-term returns than equities, resulting in lower required minimum distributions and less potential for income inclusion when you pass assets on to your heirs.

Holding the highest return investments in a Roth IRA ensures the greatest tax efficiency from an account that may never be subject to tax. That means the account should only hold equities. While it can entail more risk, you should have a long time horizon for a Roth account. That makes it better suited to handle volatile investments with the potential to produce higher long-term returns.

Having investments with greater growth potential in a Roth account provides two primary benefits.

- You don’t pay taxes on your gains.

- Your heirs won’t pay taxes on withdrawals from Roth accounts either. (Note that heirs, other than your spouse, will generally only have 10 years to withdraw money from a Roth IRA.)

There is one other factor to consider. If you sell investments held in retirement accounts at a loss, you will not realize such losses for tax purposes. Not every investment will go up in value; some are bound to decline.

Examples Showing the Benefits of Asset Location

Interest Income: Assume your target asset allocation is 70% equities and 30% fixed income. If you do not need current income from your portfolio, asset location can prove beneficial. How? Hold any fixed-income securities in your IRA. Why? You won’t pay taxes on the interest income they generate. Note that this matters a little less in today’s low-interest-rate environment

Fixed-income assets are less likely to provide meaningful growth. That leads to a second benefit. When you withdraw money from your account, your tax bill will be less. Remember that withdrawals from your IRA get treated as ordinary income. Ordinary tax rates are higher than capital gain rates.

Please don’t interpret any of this as meaning we don’t want to see your assets grow. We do. That’s always one of our objectives when we manage a client’s portfolio. Asset location relates to deciding which assets you hold in each account type. If you have more than one account type, you want to think about which type of asset belongs in which type of account.

Foreign Taxes: You are a shareholder of a French corporation. You receive a $100 refund of the tax paid to France by the corporation on the earnings distributed to you as a dividend. The French government imposes a 15% withholding tax ($15) on your dividend income. You receive a check for $85. You report the $100 as dividend income. The $15 of tax withheld represents a qualified foreign tax. You can claim the $15 of foreign taxes as a credit against the taxes owed on your dividend income. That means your tax bill will be lower.

You could deduct the foreign taxes instead, but that’s usually less favorable than a tax credit. You must itemize any foreign taxes you deduct. You also must deduct all your foreign taxes. You cannot take a credit for some and deduct others.

But you can’t deduct foreign taxes you pay on investments held in a tax-deferred retirement account. The income in those accounts is not subject to current U.S. tax (at least not until you begin making withdrawals).

But don’t worry—you won’t lose the benefit of the foreign taxes you paid in those accounts. The foreign taxes reduce the income earned in that account. It’s like you take a deduction against the income, and when you withdraw the money, you are only taxed on the net amount. It’s like claiming an itemized deduction for your foreign taxes.

If you have a Roth IRA, the situation is a bit different. Withdrawals from Roth accounts are not taxed by the IRS, so the foreign taxes you paid provide no benefits. But don’t let the absence of a tax benefit deter you from holding foreign investments in your Roth account. In some cases, it could still make sense to have foreign assets in those accounts. There are many other factors to consider apart from taxes when making investment decisions. For example, portfolio diversification and the suitability of the asset for your portfolio.

Appreciated Assets: You bought 200 shares of XYZ Inc. for $10/share. Twenty years later the shares are worth $150 each. Pat yourself on the back for deciding to buy those shares. You turned a $2,000 investment into $30,000. Assume you are in the 15% tax bracket for capital gains. You file a joint tax return, and your income is $200,000 in retirement. Nice job. You did a great job of saving for retirement, too. Your filing status is Married Filing Jointly. Let’s look at the difference in tax cost when you sell the shares and withdraw the net proceeds. Note: This analysis excludes state income tax effects:

- Shares held in a taxable account: You have a capital gain of $28,000 ($30,000 – $2,000. With a 15% tax rate, you pay $4,200 ($28,000 x 15%) of federal income taxes. Your net proceeds: $25,800 ($30,000 – $4,200).

- Shares held in your IRA: For this purpose, your gain or loss doesn’t matter. You apply your 24% tax rate to the $30,000 of sales proceeds. You pay $7,200 in taxes ($30,000 x 24%). Your net proceeds: $22,800 ($30,000 – $7,200).

- Shares held in your Roth IRA or HSA: Your gain or loss doesn’t matter for this purpose either. You pay no taxes when you withdraw the sales proceeds. (Assume you have qualified medical expenses if withdrawing funds from your HSA.) Your net proceeds: $30,000 ($30,000 – $0).

Those tax savings matter. They become even more meaningful when you apply them across an entire portfolio.

Don’t Let the Tax Tail Wag the Dog

Limiting the amount of taxes you pay is a proper approach as long as it maximizes after-tax returns. That’s the benefit tax location strategies can provide. However, remember not to make decisions solely based on tax implications. Plus, to implement such a strategy, portfolios must be managed at the household level and not on an account-by-account basis. This can add complexity. It can also make the returns in individual accounts uneven. Overall, utilizing such a strategy can allow you to benefit from lower current and future taxes.

Tax-inefficient investments typically include those providing a high expected return that is in the form of current income. Investments with the greatest potential tax liability are those that should be prioritized when considering tax-advantaged accounts.

Investors should also be aware of the tax benefits associated with certain securities. For example, municipal bonds, U.S. government securities, and MLPs provide tax benefits that make them more appropriate for taxable accounts.

Summary

Considering which account should hold which investments matters. It can help investors with both taxable and tax-advantaged accounts reduce their taxes. It often helps to consult with a professional before making asset location decisions. Suggestions in this blog may not apply to everyone as its primary purpose is providing general guidance.

Do you need help with how to apply asset location to your investments? I would be happy to schedule a call to answer your questions. Click my CALENDAR LINK to schedule a call. I enjoy discussing topics like this.

Our practice continues to benefit from referrals from our clients and friends. Thank you for your trust and confidence.

We hope you find the above information valuable. If you would like to talk to us about financial topics including your investments, creating a financial plan, saving for college, or saving for retirement, please complete our contact form. We will be in touch. You can also schedule a call or a virtual meeting via Zoom.

Follow us: Twitter Facebook LinkedIn

Please note. We post information about articles we think can help you make better money-related decisions on LinkedIn, Facebook, and Twitter.

Phil Weiss founded Apprise Wealth Management. He started his financial services career in 1987 working as a tax professional for Deloitte & Touche. For the past 25+ years, he has worked extensively in the areas of financial planning and investment management. Phil is both a CFA charterholder and a CPA.

Located just north of Baltimore, Apprise works with clients face-to-face locally and can also work virtually regardless of location.